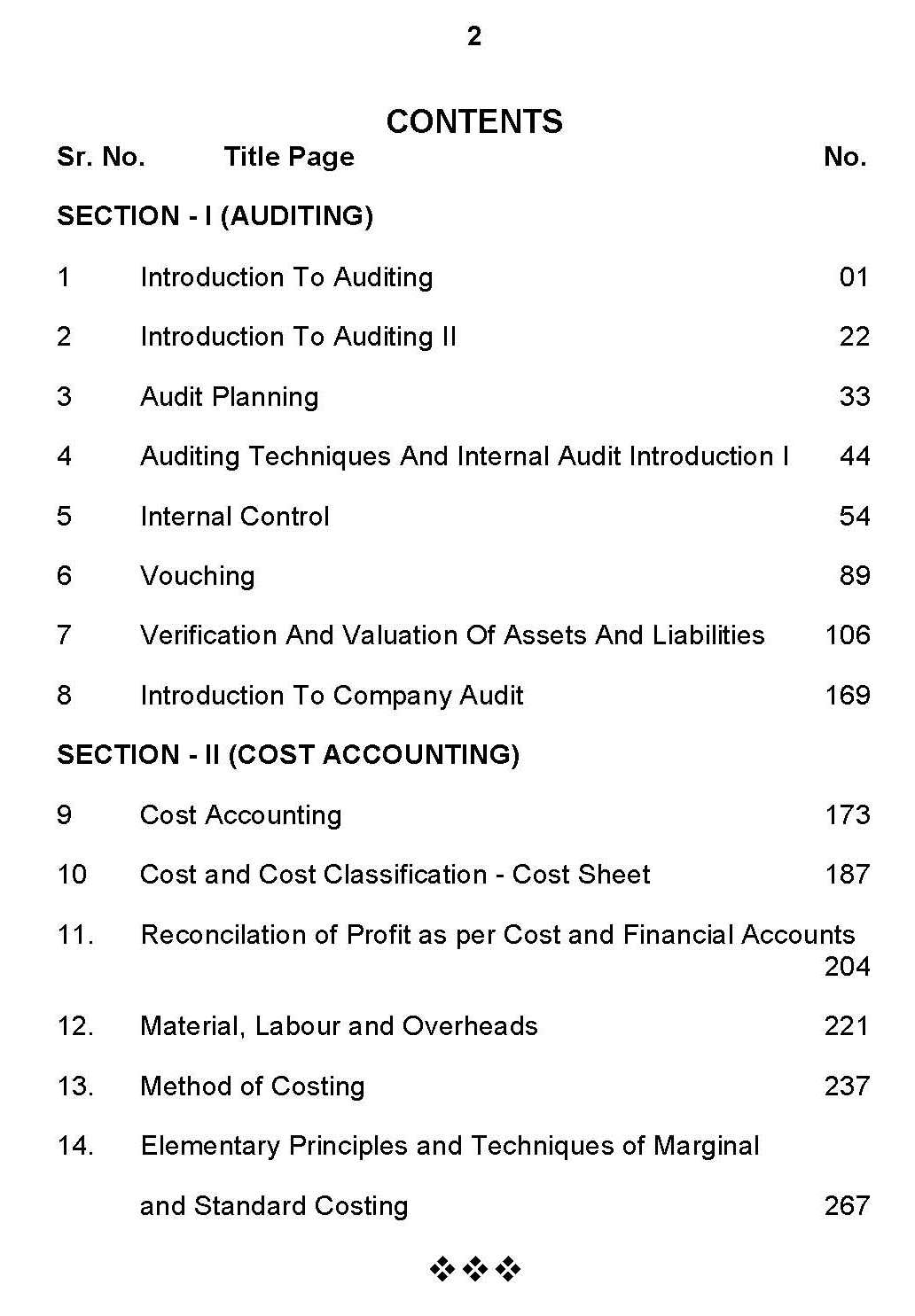

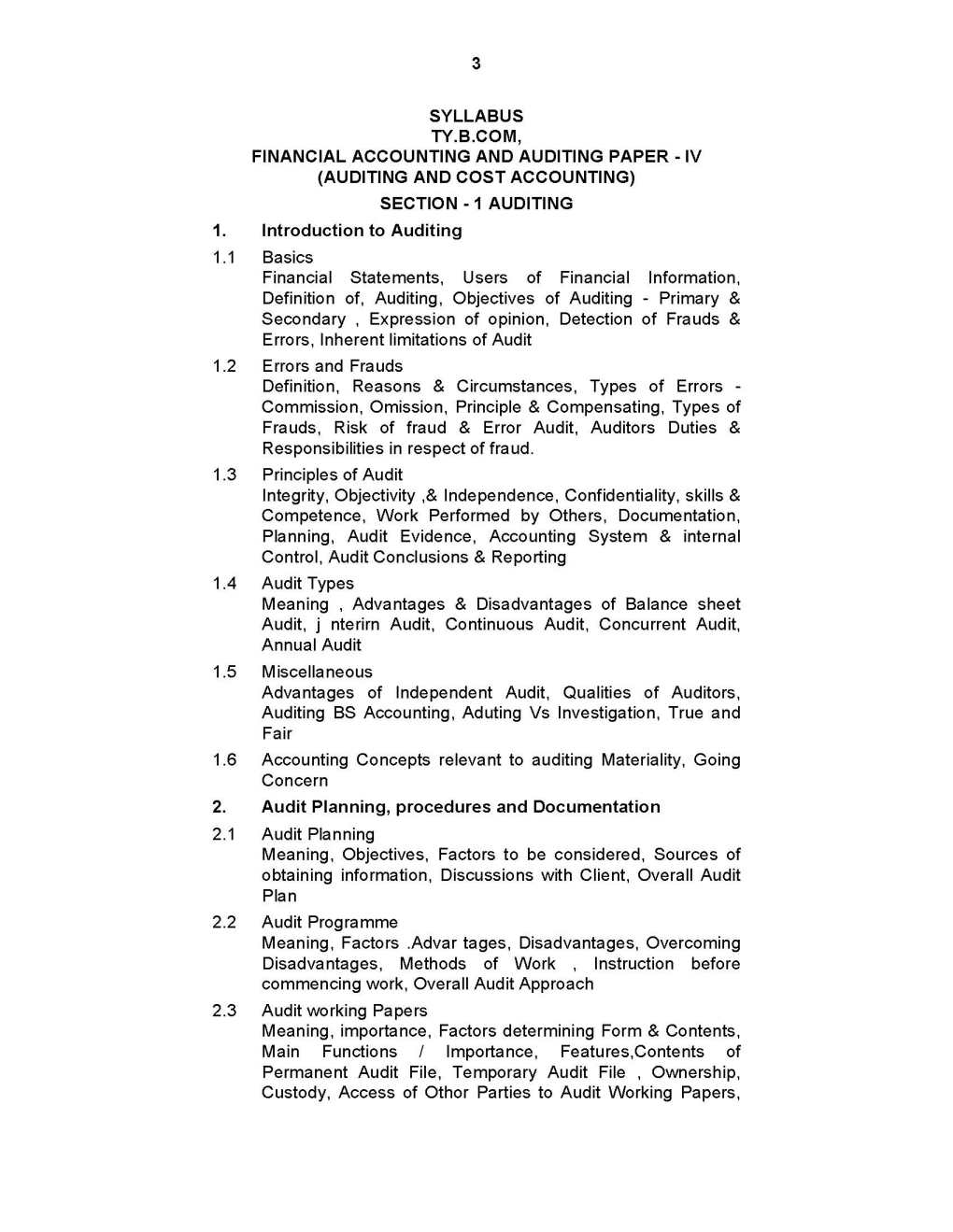

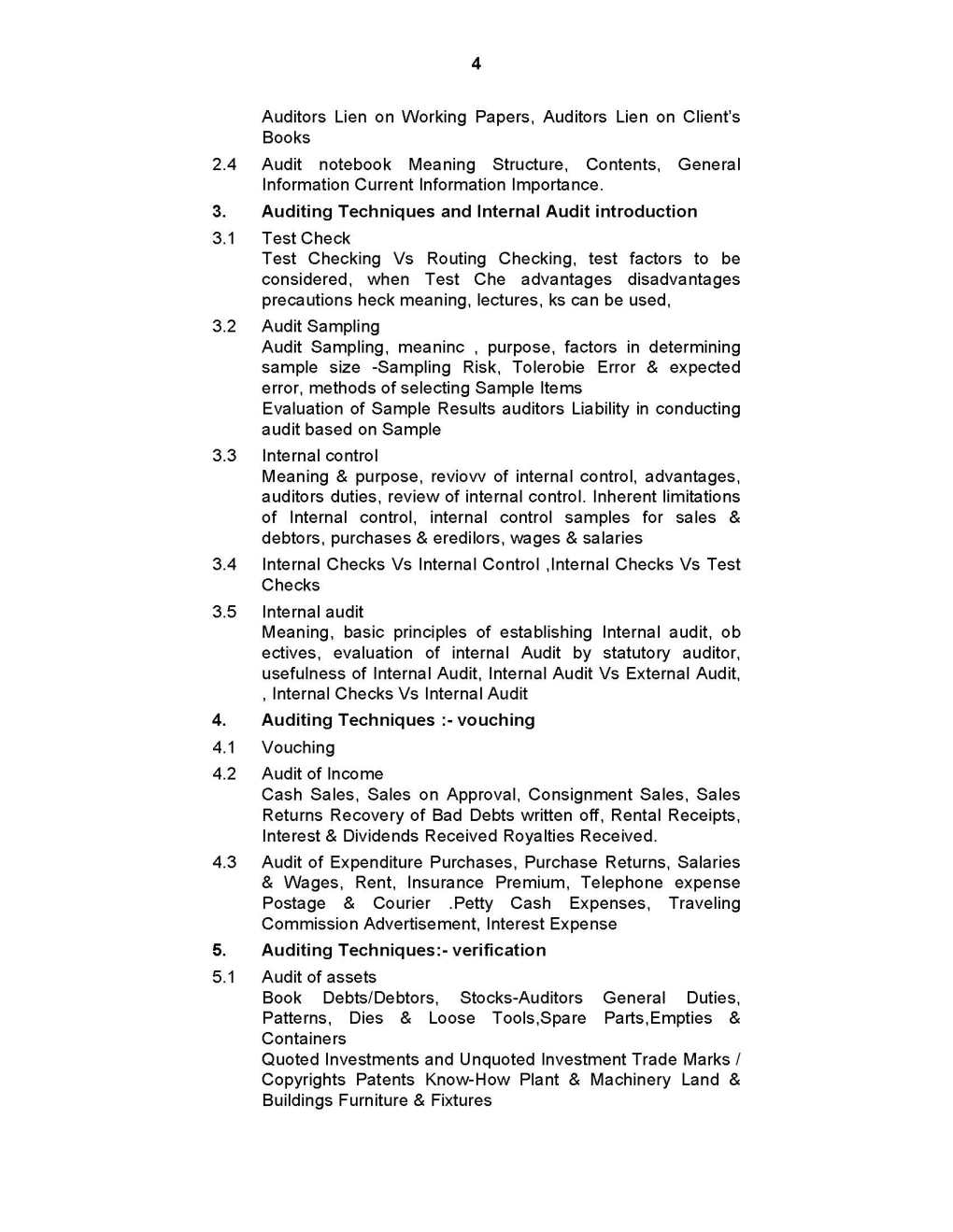

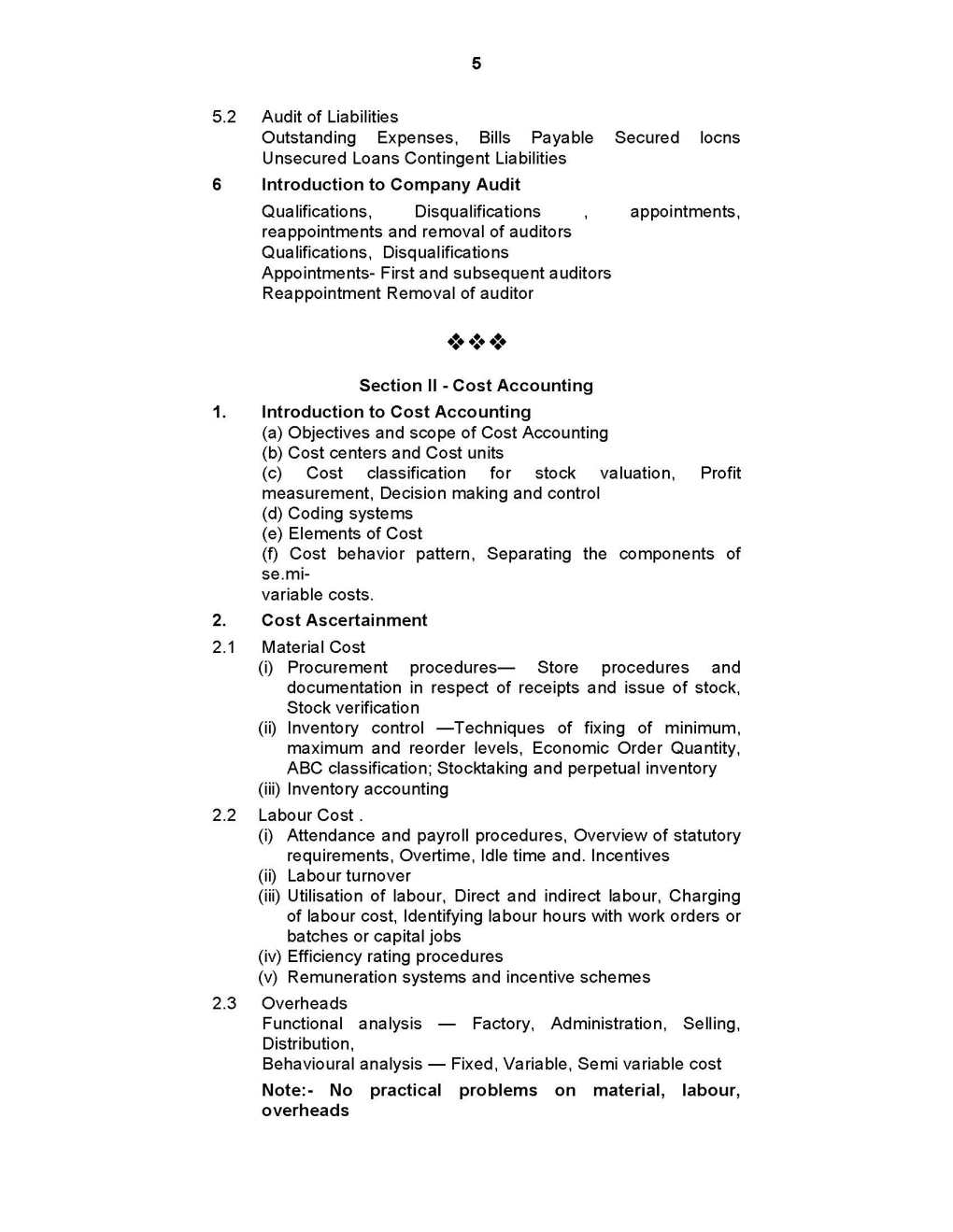

| Re: Mumbai University T.Y.B.Com Financial Accounting Exam Paper

Here is the list of few questions of T.Y.B.Com Financial Accounting exam of Mumbai University which you are looking for .

Mumbai University T.Y.B.Com Financial Accounting Exam Paper

Q.1.

Trial Balance of K. Swapnii Ltd. as on 31st March, 2007 is as below:- (20)

Particulars Dr. (Rs.) Cr. (Rs.)

16, 000 equity shares of Rs. 100 each fully paid up - -- 16,00,000

Securities Premium - -- 15,000

General Reserve -- 50,000

Gross Profit - -- 8,00,000

Discount Received -- 8,700

Creditors -- 25,800

Profit and Loss A/c. -- 20,000

Provision for Taxation (Accounting year 2005-06) -- 70,000

Interest Received (net after TDS) -- 9,500

Land (Cost) 1,55,000 --

Building 3,00,000 --

Plant and Machinery 2,50,000 --

Furniture 1,00,000 --

Vehicles 1,50,000 --

Office Salaries 1,55,000 --

Office Rent 120,000 --

Establishment Expenses 58,000 --

Finance Expenses 49,000 --

Debtors 90,000 --

Interim Dividend 80,000 --

Cash on Hand 8,000 --

Bank Balance 2,00,000 --

Security Deposit 7,800 --

Advance Tax (Accounting Year 2006-07) 1,00,000 --

Investments (5% Government Securities) 2,10,000 --

Stock-Raw Materials 1,50,000 --

Stock - Work -in-progress 1,75,000 --

Stock- Finished Goods 1,25,000 --

Advance Tax (Accounting Year 2005 - 06) 80,000 --

Selling and Distribution Expenses 36,200 --

Total 25,99,000 25,99,000

After taking into account following adjustments, prepare Profit & Loss account for the year ended

31st March,2007 and Balance Sheet as on the same date, as per Schedule VI requirements, in Vertical form:

Name Cost (Rs.) Rate %

Building 4,00,000 2.5%

Plant and Machinery 5,00,000 10%

Furniture 2,00,000 15%

Vehicles 3,00,000 20%

1. Write off depriciation on fixed Assets on the original cost of fixed assets as hereunder.

2. Market value of Investments is Rs. 2,15,000 while face value is Rs. 2,00,000.

3. Auditor's Remuneration is to be provided for the year Rs. 16,000. It includes their fees as

auditor Rs. 10,000, as consultant on Tax matters Rs. 4,000 while the remaining amount is as consultant on Company law matters.

4. Managing Directors remuneration paid Rs. 5,000 per month is included in office salaries. However, he is entitled to remuneration of Rs. 70,000 p.a..

5. Provide for salaries Rs. 8,000. Rent Rs. 10,000. Establishment Expenses Rs. 7,000 as outstanding expenses for the year.

6. General Reserve includes profit on re-issue of forfeited shares earned Rs. 5,000

7. Provision for taxation to be made Rs. 1,00,000 for current year.

8. Debtors include debts due for more than 6 months Rs. 15,000. All debts are considered to be good and unsecured.

9. The Income Tax Assessment for accounting year 2005-06 was completed resulting into gross demand of Rs. 78,000.

10. Interest received on Government Securities is after deduction of income tax of Rs. 500, for current year.

11. Ignore previous year's figures and Corporate Dividend Tax.

Q.2.

ICL Ltd. was incorporated to take over the running business of BC and CI Brothers with effect from 1st April 2006, The Company was incorporated on list August 2006. The following information was available from the books of accounts, which were closed on 31st March 2007: (16)

Particular Rs. Rs.

Gross Profit 7,00,000 --

Share Transfer Fees Received 10,0000 --

-- -- 7,10,000

Expenses:

-- --

Office Salaries -- 2,10,000

Partners' Salaries -- 60,000

Advertising -- 63,000

Printing Stationery -- 15,000

Travelling Expenses -- 40,000

Office Rent -- 96,000

Auditors' Remuneration -- 6,000

Directors' Fees -- 10,000

Bad Debts -- 12,000

Sales Commission -- 49,000

Preliminary Expenses -- 7,000

Debenture Interest -- 16,000

Interest on Capital -- 18,000

Depriciation -- 21,000

Additional Information:

1. Monthly sales were Rs. 5,00,000 for pre- incorporation period, while total sales for the year

were Rs. 70,00,000. The sales arose evenly throughout the concerned periods.

2. Office rent was Rs. 84,000 p.a.upto 30th Sept. 2006. It became Rs. 1,08,000 p.a. thereafter.

3. Travelling Expenses included Rs.7,000 towards sales promotion.

4. Auditors' Remuneration was payable for whole year.

5. Bad Debts written off included a debt of Rs. 4,000 taken over from the vendor, while the remaining were in respect of goods sold in September 2006.

6. Depreciation includes Rs. 6,000 for asset acquired in the post incorporation period.

Prepare Profit & Loss accounts for the year ended 31st March 2007 in the columnar form showing profit/loss for the pre and post incorporation period

Q.3.

Smart Company issue on 1st April, 2001, 2600, 7% Preference shares of Rs. 100 each at par redeemable on or after 31-3-2006 in whole or in past. The Company later, issued 8% debentures of the face value of Rs. 1,00,000 on 1-4-2002 redeemable on or after 3-3-2007 also in whole or in part. (16)

On 31-3-2006, the Preference shares of the face value of Rs. 1,80,000 were redeemed out ofprofits.

On 1-3-2007, the Company, for the purpose of redemption of preference shares, issued 5,000 equity shares of Rs. 10 each at a premium of 2%. All the shares were fully subscribed for.

On 31-3-2007, it redeemed the remaining preference shares at par. The company redeemed all the debentures (out of profits) also on the same date at a premium of 5%.

There was sufficient balance in General Reserve Account and Bank Account as on 31-3- 2006 and 31-3-2007.

Ignore preference dividend and debenture interest.

Pass journal entries in the books of the company for the year ended 31st March 2006 and 31 st March, 2007 for redemption of preference shares and debentures in view of provisions of Companies Act, 1956.

Q.4.

Following is the Balance Sheet of Unmesh Ltd. as on 31-3-2007: (16)

Balance Sheet as on 31-03-2007

Liabilities Rs. Assets Rs.

6,000 10% Cumulative preference -- Goodwill 2,00,000

Shares of Rs. 100 each fully paid up 6,00,000 Land Building 19,50,000

15,000 Equity Shares of Rs. 100 each, fully paid up 15,00,000 Plant and Machinery

70,000

Loans 2,22,000 Stock 4,00,000

Creditors 7,50,000 Trade Debtors 2,88,000

-- -- Bank Balance 1,26,000

-- -- Profit and Loss A/c. 38,000

-- 30,72,000 -- 30,72,000

Note:

Preference Dividend was in arrears Rs. 1,20,000

The Board of Directors of the Co. decided upon the following scheme of reconstruction, which was approved by all concerned.

1. Paid up value of equity shares shall be reduced to Rs. 50 per share, face value being Rs. 100.

2. Preference shares are to be converted into 13% debentures of Rs. 100 each with regard to their 80% of dues (including arrears of preference dividend) and for the balance (including dividend arrears) equity shares of Rs. 100 each (Rs. 50 paid up) shall be issued.

3. All equity shareholders agreed to pay the balance amount, making shares fully paid up.

4. The Plant-Machinery was revalued at Rs. 90,000.

5. The value of stock was reduced by Rs. 1,00,000

6. Land and Building shall be written down to Rs. 15,50,000.

7. Creditors agreed to forego their claims by 10%.

Loan was fully settled for Rs. 2,00,000.

8. Goodwill, Debit balance of Profit and Loss account shall be written off.

9. Cost of reconstruction Rs. 5,000 was paid. Above resolution was carried out.

You are required to :

1. Pass journal entries in the books of the company

2. Prepare Capital Reduction account.

3. Prepare Balance Sheet after reconstruction.

Q.5.

Following is the Balance Sheet of Golu Ltd, as on 31-3-2007: (16)

Balance Sheet as on 31-03-2007

Liabilities Rs. Assets Rs.

10,000 Equity Shares of Rs. 10 each fully paid up 1,00,000 Fixed Assets 4,50,000

5,000 Equity Shares of Rs. 10 each Rs. 8 paid up 40,000 Current assets 2,20,000

5,000 Equity Shares of Rs. 10 each Rs. 5 paid up 25,000 Preliminary Expense 10,000

General Reserve 2,00,000 -- --

Profit & Loss a/c. 1,80,000 -- --

Creditors 1,35,00 -- --

-- 6,80,000 -- 6,80,000

Additional Information:

1. Fixed Assets are undervalued 10%

2. Current Assets are overvalued by 10%.

3. The normal average profit of the Co. after tax will be maintained at Rs. 99,000.

4. Normal Rate of Return is 10%.

Calculate the value of each type of equity share by,

(i) Asset Backing Method (excluding Goodwill).

(ii)Yield Value Method

Q.6.

Journalise the following transactions in the books of EXIM Ltd. for the year ended 31-3-2007 and also prepare "Foreign Exchange Fluctuation Account" applying AS-11.- (16)

(a) On 1st July, 2006, goods worth US $ 1,05,000 were exported to M/s. Pasco Ltd. The amount was realised as below:

Date Amount Paid in US $

5-11-2006 70,000

11-5-2007 35,000

(b) Goods worth US $ 5,000 were exported on 15-7-2006 to Joe Co. Ltd, USA. The amount was received after 30 days.

(c) On 15-9-2006, Raw Materials worth US $ 20,000 were imported from Robert Ltd. Payable 50% immediate and the balance on 15-4-2007.

(d) Raw Materials were imported on 31-10-2006 worth US $ 10,000 from Blue Cross Ltd. U.K. The payment wasmade after 45 days.

(e) On 15-12-2006 Goods worth US $ 75,000 were exported to Thomas Ltd., UK. The amount was received as below:.

Date Amount Paid in US $

15-2-2007 30,000

15-3-2007 45,000

(f) Plant & Machinery was imported from California Equipments Ltd. on 1-1- 2007 for US $ 14,000. The Payment for the same was made on 30-4-2007.

The Exchange Rates for 1 US $ were as below:

Balance Sheet as on 31-03-2007

.

Date Exchange Rate Rs. Date Exchange Rate Rs

01-07-2006 41.00 01-01-2007 42.25

15-07-2006 41.25 15-02-2007 42.50

14-08-2006 41.50 15-03-2007 42.75

15-09-2006 41.00 31-03-2007 42.00

31-10-2006 41.75 15-04-2007 42.50

05-11-2006 40.00 30-04-2007 42.75

15-12-2006 42.00 11-05-2007 42.00

Q.7.

Balance Sheet of North Sick Ltd. as on 31-03-2007 is as below:- (16)

Liabilities Rs. Assets Rs.

5,000 8% Preference Shares of Rs. 10 each 50,000 Office Premises --

fully paid up -- At Goregaon 1,00,000

25,000 Equity Shares of Rs. 10 each fully paid up 2,50,000 At Borivli 60,000

10% Debentures 50,000 Furniture 40,000

Creditors 40,000 Current Assets 1,90,000

-- 3,90,000 -- 3,90,000

A new Company namely West Healthy Ltd. was formed with Authorised Capital of 50,000 equity shares

of Rs. 10 each. The directors of the Company.

(a)Issued 10,000 equity shares at premium of 10% to the public for cash. The issue was fully subscribed and paid for.

(b)Paid underwriting commission of Rs. 5,000 to the underwriters ICICI Bank Ltd.

(c)Paid Rs. 10,000 to M/s. ANIC & Co. Chartered Accountants, as professional fees for Co. formation.

(d)Decided to take over the business of North Sick Ltd. on the following terms:

(i) To issue 6 equity shares of Rs. 10 each at 10% premium for every 5 equity shares in North Sick Ltd.

(ii) To issue 5,000 equity shares of Rs. 10 each at 10% premiumto the preference shareholders of North Sick Ltd.

(iii) To revalue Goregaon Office at Rs. 1,50,000 and BorivliOffice at Rs. 90,000

(iv) To take over 10% debentures of North Sick Ltd. at facevalue. Then, debentureholders of North Sick Ltd. shall be issued 12% debentures of the face value Rs. 55,000 in West Healthy Ltd.

You are required to :

Write necessary journal entries in the books of West Healthy Ltd. to record the above transactions.

Prepare Balance Sheet of West Healthy Ltd. as on 1-4-2007, after take-over.

Q.8.

On 1-4-2006 Mr. Abhishek had 10,000 equity shares (of Rs 10 each) in Rai Entertainment Ltd-at the cost of Rs. 1,60,000:- (16)

On 1-7-2006 he acquired 4,000 more shares in the same Company for Rs.80,000

On 31-7-2006 he further acquired 6,000 more shares at Rs. 22 per Share

On 10-8-2006 Rai Entertainment Ltd.announced bonus share to the then equity shareholders In the ratio of 1 bonus Share for every 4 shares held as on 5-8-200 6. Abhishek received the bonus shares on 22-8-2006.

The directors of Rai Entertainment Ltd. issued right shares to the equity shareholders on the following terms:

(a) Right shares to be issued to-the existing shareholders as on 31-8-2006.

(b) Right offered was at the rate Of Rs. 15'per share in the ratio 1 share for every 5 shares held. Full amount was payable on or before 15-10-2006.

(c) Shareholders would be entitled to renounce their entitlement either wholly or in part to the outsiders.

(d) Abhishek exercised his right of option under the issue for 3,000 shares and sold the balance to Mr. Raj @ Rs. 4 per share. On, 20-10-2006 Rai-Entertainment Ltd. declared the dividend @ Rs. 4 per share for the year ending 31-3-2006.Abhishek received the dividend on 31-10-2006. On 10-1-2007 Abhishek sold 7,000 shares @ Rs. 40 per share. Prepare investments a/c. in the books of Abhishek for the year ended 31-3-2007.

Q.9.

Attempt any four of the following :- (16)

a. Following information is available from the books of a Company:

-- Rs.

1,20,000 equity shares of Rs. 10 each 12,00,000

Security premium 70,000

General Reserves 3,50,000

The Company decided to buyback 25% of the equity share capital at Rs. 12 per share. Pass journal entries without narration.

b. Bharat Ltd. issued 50,000 15% Debentures of Rs. 1000 each at Rs. 952 per debenture. The debentures are redeemable in five annual instalments of Rs. 200 each. It is decided to write off discount on debentures in proportion to the amount of debenture finance usage over a period of five years.

Prepare a statement for write off at discount on debentures over a period of five years.

c. Profit before making the following adjustment were as under:

-- Pre-incorporation period

Rs. Post-Incorporation period Rs.

Profit 37,000 18,600

Adjustments to bemade:

The Purchase consideration was agreed at Rs. 2,50,000 for assets valued at Rs. 2,40,000. 20% of the Goodwill is to be written off.

In lieu of interest on purchase consideration the vendor would get 40% of the profit earned prior to incorporation.

Find out profit prior to incorporation and after incorporation.

Determine the no. of fresh issue of shares for the purpose of redemption of preference share, from the following information.

-- Rs.

Nominal value of redeemable preference share capital 1,50,000

Premium on redemption of preference shares 10%

Profit & Loss account (Cr. balance) 34,000

Securities Premium 5,000

Fresh issue is to be made at 5% premium. Face value of each share is Rs. 100.

(e) The net profits of a company after Tax for the past five years are Rs. 40,000, Rs. 42,000, Rs. 45,000, Rs. 46,000 and Rs. 47,000 average capital employed is Rs. 4,00,000 on which a reasonable rate of return is 10%. It is expected that the company will be able to maintain its super profits for the next five years. Calculate the value of Goodwill on the basis of annuity of super Profits, taking the present value of annuity of one rupee for five years @ 10% interest is Rs. 3.78.

(f) 9% debentures (of Rs. 100 each) account in the books of a company shows the balance of Rs. 5,000 of Rs. 5,00,000 as on 1-1-2006.

It purchased its own debentures as under:

On 1-2-2006 - 500 debentures @ Rs. 98 - Cum interest.

On 1-3-2006 - 700 debentures @ Rs. 96 Ex-interest.

Pass journal entries for the purchase of own debentures and immediate cancellation thereof.

Interest was payable on 30th June and 31st December every year.

Q.1 BK Ltd. is formed to takeover 'Bunty Ltd and Kuber Ltd'. Their Balance Sheets on the date of amalgamation are as below: 16

Liabilities Bunty Ltd.Rs. Kuber Ltd.Rs. Assets Bunty Ltd.Rs. Kuber Ltd.Rs.

Share Capital of -- -- Goodwill -- 25,000

Rs.10 each -- -- Buildings 1,50,000 1,40,000

Equity shares 2,40,000 1,60,000 Machinery 80,000 60,000

11% Preference Shares 1,50,000 1,00,000 Furniture 10,000 5,000

General Reserve 45,000 40,000 Investments 1,40,000 80,000

Profit & loss A/C 30,000 21,000 Debtors 1,65,000 60,000

9% Debentures 1,00,000 1,00,000 Stock 75,000 90,000

Sundry Creditors 60,000 40,000 Cash & Bank 13,000 8,000

Other Liabilities 40,000 24,000 Other Current Assets 20,000 10,000

-- -- -- Preliminary Expenses 12,000 7,000

-- 6,65,000 4,85,000 -- 6,65,000 4,85,000

BK Ltd. issued 10,000 equity shares of Rs.10 each to the public at a premium of 10%.Bunty Ltd. and Kuber Ltd. were taken over by BK Ltd. on the following terms.

Re: Bunty Ltd.

1. Equity Shareholders are to be issued 7 Equity Shares of Rs. 10 at par in BK Ltd. and are to be paid Rs.5 in cash for surrender of each 6 Shares.

2. Preference shareholders are to be paid at 10% premium by 12.5% preference shares in BK Ltd. issued at par.

3. All Assets and liabilities are valued at book value except Machinery which is valued at 10% below book value and Debtors are Debtors are worth Rs. 1,60,000.

4. Liquidation expenses of Rs.12,500 are to be borne by BK Ltd.

5. Discharge the debentures of Bunty Ltd. at a discount of 10% by the issue of 13% Debentures of Rs.100 each in BK Ltd.

Re: Kuber Ltd.

1. Cash Rs.3,000 is to be retained for liquidation expenses.

2. Debtors and investments are valued at 90% of cost.

3. Machinery and stock are valued at 10% above cost and other assets and liabilities are valued at book value except Fictitious assets.

4. Prefrence shareholders are to be paid at 10% premium by 12.5% prefrence shares in BK Ltd. issued at par.

5. Balance of Purchase consideration is payable,in equity share at par.

6. Discharge the debentures of Kuber Ltd. at par by the issue of 13% Debentures of Rs.100 each in 'BK' Ltd.

7. The Face value of Equity shares and preference shares in BK Ltd. is of Rs.10 each.

Show the necessary Ledger Accounts in the books of 'Bunty Ltd' and Kuber Ltd'.also calculate purchase considerations.

Q.2 The following trial balance was extracted from the books of M/s. Jhakharia Pvt. Ltd., which had taken over business of Mr. Vardhan on 1st April, 2005. The company was incorporated on 1st July, 2005. However no effect of conversion was given in the books which continued thereafter. 16

Trial Balance as on 31st March, 2006

Trial Balance as on 31st March, 2006

Particular Debit Rs. Credit Rs.

Capital Account of Mr. Vardhan on 1/4/05 ---- 9,00,000

Debtors 80,000 ----

Creditors ---- 1,00,000

Rent 33,000 ----

Office Salary 1,10,000 ----

Carriage outward 54,000 ----

Directors Remuneration 16,000 ----

Travelling Expenses 28,500 ----

Preliminary Expenses 15,000 ----

Administrative Expenses 1,60,000 ----

Bills Receivable 30,000 ----

Bills payable ---- 21,500

Cash at Bank 60,000 ----

Plant & Machinery 2,00,000 ----

Land & Buildings 5,00,000 ----

Furniture 40,000 ----

Stock 1,90,000 ----

Gross Profit ---- 4,95,000

Total : 15,16,500 15,16,500

Further Information:

1. Gross Profit percentage is fixed. Turnover is doubled in April, November and December as compared to other months.

2. 1/5 of preliminary expenses are to be written off.

3. Purchase consideration Rs. 10, 00,000 to be paid by the issue of 80,000 equity shares of Rs. 10/-each and 2,000 9% preference shares of Rs. 100/- each.

4. Travelling expenses are incurred by, salesmen only.

5. Audit Fee is Rs. 18,000/- for 1st April, 2005 to 31st March, 2006 and is outstanding.

6. Rent of office was paid @ Rs. 2,500/-, per month up to September, 2005 and thereafter, it was increased by Rs. 500/- per month.

7. Provide depreciation @ 10% p.a. on Plant & Machinery, Land & Building and on Furniture.

Prepare profit and loss account for the year ended 31st March, 2006 appropriating between the pre and post incorporation period and Balance Sheet as on 31st March, 2006.

Q.3 The following is the Balance-sheet of Sandeep Limited as on 31st March, 2006: 16

Liabilities Rs. Assets Rs.

Issued and Subscribed Capital -- Goodwill 25,000

10% Preference Shares of -- Patents 15,000

Rs. 100/- each 4,00,000 Furniture 35,000

Equity Shares of Rs. 10/- each 10,00,000 Plant & Machinery 6,00,000

12% Debentures 7,50,000 Land & Building 6,50,000

Bank Overdraft 50,000 Stock-In-Trade 80,000

Sundry Creditors 1,40,000 Sundry Debtors 90,000

Bills Payable 35,000 Bills Receivable 15,000

-- -- Profit and Loss A/c 8,20,000

-- -- Preliminary Expenses 45,000

-- 23,75,000 -- 23,75,000

The preference dividend is in arrear for four years. The following scheme of capital reduction was sanctioned by the court and agreed by shareholders:

1. The preference shares are to be reduced to Rs. 50/- each and equity shares to Rs. 2/- each, both being fully paid.

2. Of the preference dividend in arrear three-fourth to be waived and remaining to be paid in cash.

3. The Debenture holders to take over plant and machinery at Rs. 6, 50,000/- in part satisfaction of their claim. The remaining claim should be converted into 14% debentures.

4. Creditors agreed to reduce their claim by Rs. 20,000/-. Bills payable to be paid immediately.

5. Goodwill, Patents, Profit and Loss A/c and Preliminary Expenses are to be written off entirely.

6. The following assets are to be revalued as under Furniture Rs. 25,000/-, Stock-In-Trade Rs. 68,000/- Land and Building Rs. 5, 80,000/- Sundry Debtors Rs. 80,000/-.

7. A Secured Loan of Rs. 1,50,000/- at 12% per annum is to be obtained by mortgaging Land and Building for repayment of bank overdraft, bills payable and reconstruction expenses Rs. 15,000/-.

Pass journal entries to record above scheme and draft the balance sheet of Sandeep Limited after reconstruction.

Q.4 'Piyusha' Limited furnishes the following information and requests you to find out the value of on the basis of capitalisation of Future Maintainable Profits method 16

(a) Balance Sheet as on 31st March, 2006:

Liabilities Rs. Assets Rs.

Share Capital -- Goodwill 60,000

7,500 equity shares -- Land & Machinery 7,00,000

of Rs. 100/- each 7,50,000 Plant & Machinery 2,50,000

Reserves -- 10% Investments 4,50,000

Profit & Loss A/c 3,50,000 Debtors 2,60,000

Capital Reserve 1,50,000 Stock-In-Trade 2,40,000

Workmen Compensation Fund 3,00,000 Cash and Bank 1,30,000

10% Debentures 3,00,000 Other Current Assets 1,10,000

Creditors 2,30,000 Preliminary Expenses 20,000

Other Current Liabilities 1,40,000 -- --

-- 22,20,000 -- 22,20,000

(b) In similar business normal returns on capital employed is 15% (After Tax)

(c) All Investments are Non-Trade Investments.

(d) Profits for last four years before tax are follows.

Year ending 31st March, 2003 Rs. 4, 32,000

Year ending 31st March, 2004 Rs. 4, 46,000

Year ending 31st March, 2005 Rs. 4, 36,000

Year ending 31st March, 2006 Rs. 4, 53,000

(e) An average rate of 40% is payable as Income Tax.

(f) In the year 2003-04, there was a fire which resulted in a loss of Rs. 25,000/- and during theYear 2004-05 the company had sold its furniture resulting into a profit of Rs. 40,000/-

(g) The changes expected from ensuing year are:

Increase in Directors' fees @ Rs. 12,000/- per annum.

Reduction inAdvertisement Expenses @ Rs. 42,000/- p.a.

Increase in Distribution Expenses @ Rs. 48,000/- p.a.

(h) All current Assets (excluding cash & Bank) are to be valued at 125% of book value for valuation of Goodwill).

(i) The market value of Land and Buildings is Rs. 9, 50,000/- and Plant and Machinery is Rs. 2, 00,000/

(j) Liability under workmen compensation fund is expected at Rs. 1, 50,000/-.

(k) Use Simple Average.

Q.5 Following is the Balance sheet of RT Ltd. as on 31st March, 2006: 16

Liabilities Rs. Assets Rs.

Share Capital -- Plant and Machinery 4,00,000

10,000 equity shares -- Land and Buildings 4,00,000

of Rs. 10/- each 1,00,000 Investments 2,00,000

5,000 9% preference -- Stock 60,000

Shares of Rs. 100/- each -- Debtors 1,40,000

fully paid 5,00,000 -- Bank 1,90,000

(-)call in Arrears 10,000 4,90,000 -- --

General Reserve 3,00,000 -- --

Securities Premium 20,000 -- --

Profit & Loss A/c 50,000 -- --

10% Debentures 2,50,000 -- --

Creditors 1,40,000 -- --

Bills Payable 40,000 -- --

-- 13,90,000 -- 13,90,000

On the date of Balance Sheet preference shares are redeemable at premium of 10%.

The calls in arrears on preference shares are @ Rs. 20/- per share.

1. To enable redemption, company took the following measures:-

2. To send reminders for calls to all preference share holders. Holders of 400 preference shares paid of their dues and remaining shares are forfeited and cancelled3. Sold off investments @ 110% of cost.

4. 20,000 Equity shares, of Rs. 10/- each were issued for cash consideration at 20% premium. The issue was fully subscribed and paid for.

5. The company then issued bonus shares at par to the then shareholders after issue of new shares, at the rate of three shares for every four shares held.

Pass necessary journal entries in the books of RT Ltd. for the above transactions and also prepare the Balance Sheet of the company after redemption.

Q.6 Following is the Trial Balance from the books of Diksha Ltd. as c- 31st March, 2006 :- 16

Debit Rs. Credit Rs.

Land & Buildings (at cost) 4,00,000 Share Capital --

Plant & Machinery (at cost) 5,20,000 50,000 Equity Shares of --

Motor Car (at cost) 1,00,000 Rs. 10 each 5,00,000

Goodwill (at cost) 2,60,000 8% Debentures (01-04-2005) 4,00,000

Salaries and Wages 72,000 Provision for Tax 70,000

Rent and Taxes 18,000 (Accounting year 2004-05) --

Travelling Expenses 16,000 Sundry Creditors 90,000

Printing & Stationery 17,000 Bills Payable 40,000

Motor Car Expenses 8,000 General Reserve 1,80,000

Repairs (Machinery) 16,500 Securities Premium 20,000

Stock 9 4,000 Capital Reserve 1 5,000

Debtors 1,45,000 Profit & Loss A/c (on 01-04-2005) 55,000

Cash 8,000 Provision for Depreciation (on 01-04-2005) --

Bills Receivables 30,000 (i) Land & Buildings 40,000

10% Investments 1,50,000 (ii) Plant & Machinery 1,30,000

Interest on Debentures 1 6,000 (iii) Motor Car 10,000

Advance Tax -- Gross Profit 4,10,000

For-2004-05(F.Y) 72,000 Interest on Investments 7,500

For-2005-06(F.Y) 60,000 Sale of Motor Car 35,000

-- 20,02,500 -- 20,02,500

Adjustments:-

1. Motor Car was sold on 1st April, 2005. The cost of sold Motor Car was Rs. 30,000/- and Accumulated depreciation on 1st April, 2005 was Rs. 6,000/- on the same.

2. Depreciation is to be provided on written down value at (i) Land and Building 21/2% p.a., (ii) Plant and Machinery 10% p.a. and (iii) Motor Car 20% p.a.

3. Debtors include debts due for more than 6 months Rs. 20,000/-.

4. Plant & Machinery includes machinery worth Rs. 20,000/- Purchased on 1st April, 2005.

5. Dividend is proposed for the year @ 10%, Ignore tax on proposed dividend.

6. Provision for Taxation is to be made @ 40% on the current year's profit

7. Debentures are secured by a charge on the Land and Buildings

8. The market value of Investments on 31-03-2006 was Rs. 1, 80,000/-.

9. Interest on Investment is due for 6 month but not received.

10. Interest on debentures for 6 months is Accrued & due.

11. Authorised share capital of the company is Rs. 10, 00,000/- divided into 1, 00,000/- Equity shares of Rs. 10 each.

You are required to prepare Profit & Loss Account for the year ended 31st March, 2006 and Balance Sheet as on that date in a vertical form as per provision of the schedule VI. Ignore previous year's figures.

Q.7 Following is the Trial Balance from the books of Diksha Ltd. as c- 31st March, 2006 :- 16

Date No. of Debentures Terms

01-04-2005 800 Opening Balance at a cost of Rs. 76,000/-

01-06-2005 300 Sold at Rs. 105/- each cum-interest

01-09-2005 700 Purchased at Rs. 98/- each Ex-Interest

01-12-2005 400 Purchased at Rs. 108/- each Cum-Interest

01-02-2006 900 Sold at Rs. 97/- each Ex-Interest.

Adjustments:-

Prepare Investment Account of 12% Debentures in the books off Bhagwati for the year ended 31st March,2006. The market value on 31st March, 2006 was Rs. 67,500 of the said Investment. Apply AS-13

Q.8 a) Pass journal entries for the following Foreign Exchange transactions the books 'Deepali Ltd. On 1st January, 2006 Deepali Ltd., an importer,purchased $ 42,500/- worth goods from Tom Trading Company of USA. The payment was made as under. 16

On 15thJanuary, 2006- $ 8,000

On 15th February, 2006- $9,000

On 15th March, 2006- $14,500

On 15th April, 2006- $11,000

Deepali Ltd. closes its books on 31st March every year the exchange rate for $ 1 was as follows.

1st January, 2006 Rs. 48.50 15th January, 2006 Rs. 49.25

15th February, 2006 Rs. 48.25 15th March, 2006 Rs. 48.40

31 st March, 2006 Rs. 48.75 15th April, 2006 Rs. 48.60

(b)Pass journal entries for the following transactions in foreign currency in the books of 'Priyanka Ltd.

Priyanka Ltd. exported goods to 'Jerry Trading Company' Germany worth US $ 90,000/- on 10th January, 2006 on which date

exchange rate of US $ 1 was Rs. 49.50. The payment for the same was received as under :–

Date of Payment US $ Received Exchange Rate for 1 US $

25th January, 2006 25,000/- Rs. 49.75

23rd February, 2006 24,000/- Rs. 48.90

24th March, 2006 24,000/- Rs, 48.60

28th April, 2006 17,000/- Rs. 48.90

'Priyanka Ltd' closes its books on 31st March every year. The exchange rate on 31 st March, 2006 was 1 US $ Rs. 48.75.

Q.9 Answer the following:- 16

Adjustments:-

1. 'S' Ltd is to be taken over by 'R' Ltd. 'S' Ltd. has 9% Debentures of Rs. 100/- each of the face value of Rs. 22,50,000/-. 9% debenture holders of 'S' Ltd. are dischanged by 'R' Ltd. issuing such number of its 15% Debentures of Rs. 100/- each so as to maintain the same amount of interest. Calculate the No. of debentures to be issued by 'R' Ltd. (4)

2. What amount should be set aside to get Rs. 15, 00,000 at the end of 10 years? The amount is expected to earn 4% interest. Sinking Fund Table shows that Re. 0.083290 @ 4% interest will accumulated Re. 1 at the end of 10th year. (2)

3. Prepare a -Schedule of Current Liabilities and provision" giving all the details required under Schedule VI to the Companies Act .(4)

4. 'P' Ltd. Purchased premises worth Rs. 22, 56,000. It issues its debentures at 4% discount insatisfaction of the purchase price. Calculate how many debentures will be issued in case debenture is of Rs. 100/- each. (2)

5. 'A' Ltd. buys its own 6% Debentures of nominal value Rs. 60,000/- at Rs. 97 cuminterest on 1st March, 2006. Company cancels these debentures on 31st March, 2006. Pass journal entries in the books of 'A' Ltd. It pays debentures interest half yearly on 30th June and 31st December. Face value of Debenture is Rs. 100/- each .(4)

|