|

#2

7th January 2016, 09:14 AM

| |||

| |||

| Re: CLAT Illustration

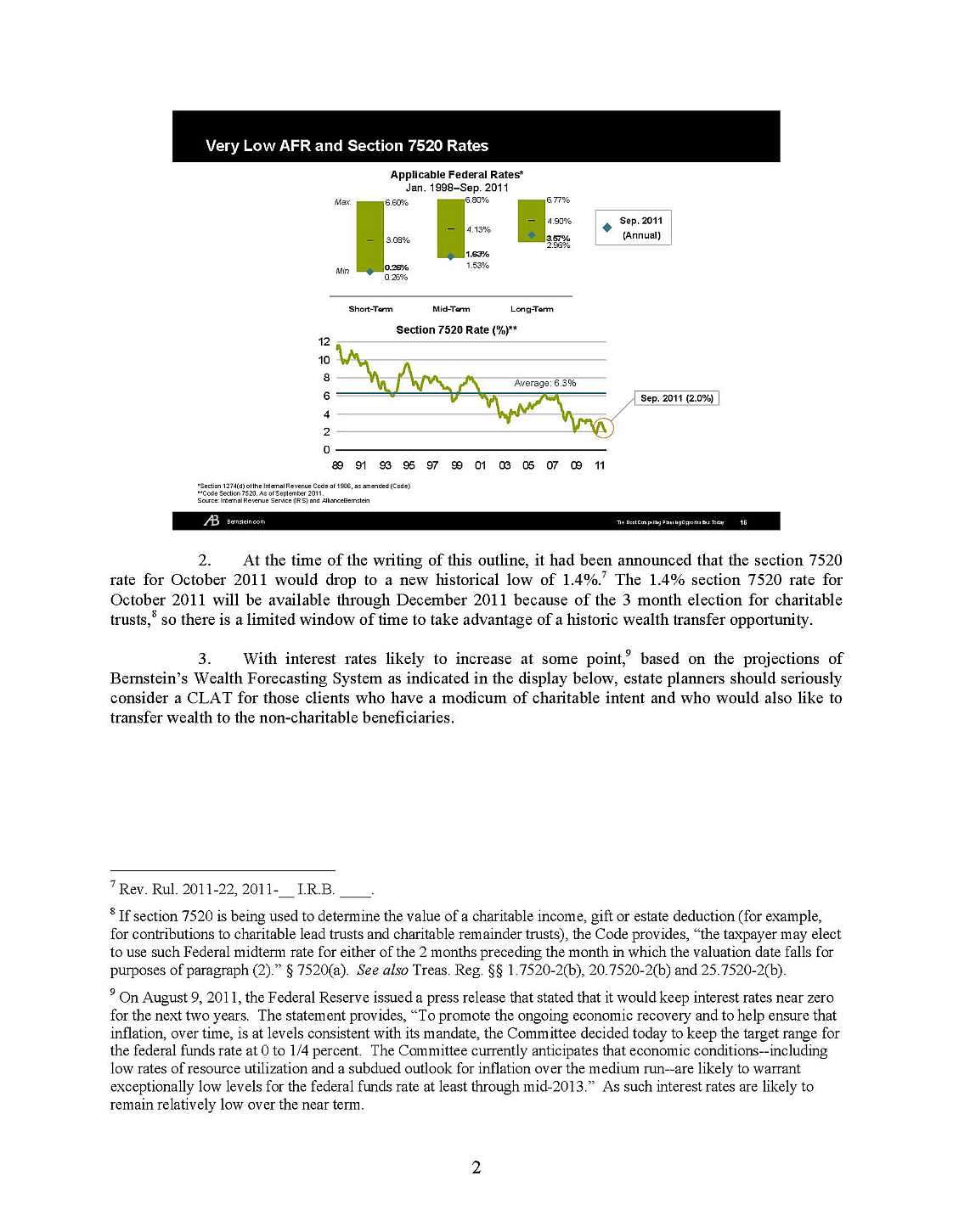

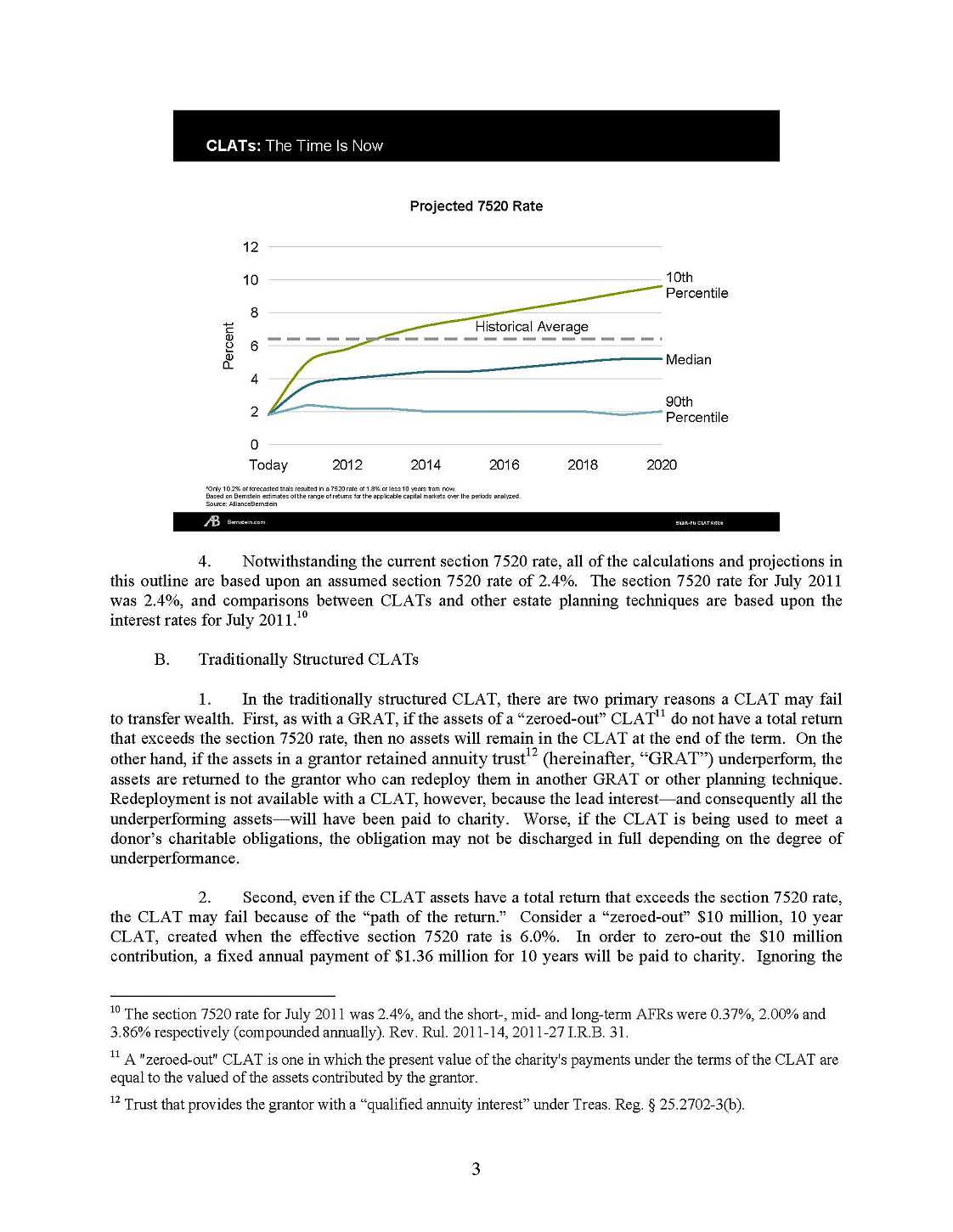

As per your request here I am providing you information about the CLAT Illustration/ structures. Here I am telling you about it as you want. Below I am providing you a file, which is containing following as you want; INNOVATIVE CLAT STRUCTURES: PROVIDING ECONOMIC EFFICENCIES TO A WEALTH TRANSFER WORKHORSE TABLE OF CONTENTS I. BACK-LOADED ANNUITY AND “SHARK-FIN” CLATS A. Introduction B. Traditionally Structured CLATs C. The GRAT Regulations D. Revenue Procedure 2007-45 E. How Extreme of a Shark-Fin is Allowable? II. FORECASTED RESULTS AND PLANNING IMPLICATIONS A. Forecasted Investment Results for Non-Grantor CLATs B. Forecasted Investment Results for Grantor CLATs III. TERM OF THE CHARITABLE LEAD INTEREST A.Term of Years B.Lifetime Terms and Mortality Risk C.Purchasing the Charitable Lead Interest IV. HIGHER SECTION 7520 RATES V. IS A SHARK-FIN ADVISABLE? VI. “INTENTIONALLY-DEFECTIVE” GRANTOR CLATS A. Introduction B. What Grantor Trust Power? C. Using Appreciated Property to Pay Charity D. Grantor to Non-Grantor Trust Status 1. Introduction 2. Income Tax Consequences 3. Recapture 4. Remaining Section 642(c) Deduction 5. Income Tax Planning: Grantor to Non-Grantor Trust Status VII. PRIVATE FOUNDATION RULES A. Generally B. Governing Instrument Language C. Self-Dealing D. Excess Business Holdings E. Jeopardy Investments VIII. NON-CHARITABLE BENEFICIARIES AND THE GST TAX EXEMPTION A. GST Tax Exemption with CLATs B. CLATs vs. CLUTs for the Benefit of Grandchildren Today IX. INVESTMENT IMPLICATIONS AND PLANNING EXAMPLES A. Generally B. FLP Interests Holding Commercial Real Property C. Private Equity Interests D. Preferred Investment FLP Interests E. Single Stock or Concentrated Stock Positions F. Life Insurance 1. Introduction 2. Basics of the Plan 3. Charitable Split-Dollar Rules X. CONCLUSION      |